By Russ and Tiña De Maris

Imagine signing a purchase contract for a new RV. You agree to 20 years of payments, but five years down the road, you find out at the end of ten years, you don’t have 10 more years of payments. Rather, there’s a whopping “balloon payment” for the rest of the note – to be paid on one month. According to authorities in Utah, that’s happened to DOZENS of customers of Utah’s General RV. Four slick employees fraudulently cooked paperwork – but no charges will be filed. Outrageous? Read on.

“Smudged” paperwork

We reported on this story when it broke in mid-May. The unfortunate customer who broke the news was Lisa Pueblo, a Farmington, Utah, resident. Lisa signed the papers for a new motorhome in 2015. It wasn’t until 2021 she found out that her 240-payment contract held by the bank was actually a 119-month contract. After that, a final red-hot payment of $63,000 to be made after the first, swallowable 119 payments. How did it happen?

A closer look at the carbon copies of the loan papers from General RV showed information of the number of payments to be made. That box showed a faint “240” – twenty years’ worth. But over the faint 240 was a much darker “119” plus a single balloon payment. Lisa was aghast. She let a major area TV station know of the problem, and they broadcast the information to their listeners in May. Apparently other General RV customers saw the broadcast and, very quickly, three more RV buyers stepped forward with so-called “smudged” paperwork. Each one was on the hook for a much-unexpected balloon payment.

A closer look at the carbon copies of the loan papers from General RV showed information of the number of payments to be made. That box showed a faint “240” – twenty years’ worth. But over the faint 240 was a much darker “119” plus a single balloon payment. Lisa was aghast. She let a major area TV station know of the problem, and they broadcast the information to their listeners in May. Apparently other General RV customers saw the broadcast and, very quickly, three more RV buyers stepped forward with so-called “smudged” paperwork. Each one was on the hook for a much-unexpected balloon payment.

The DMV investigates

The state agency in charge of investigating alleged fraud by RV dealerships is Utah’s DMV. When the story broke out, RVtravel.com contacted Allan Shinney of the DMV – the man in charge of such investigations. While Shinney was initially forthcoming, his office suddenly went mum. Nothing further came from the DMV until just this month – and it’s not good news. The DMV has investigated and say four General RV employees cooked the paperwork, but they won’t be charged.

Interestingly, none of the four “paper cookers” works for General RV anymore. Nor would the DMV release the names of those they suspect were responsible for what we deemed “perverted paperwork.” So why are these frauds free to go? Blame it on Utah’s statute of limitations. Under state law, charges against crimes of this nature must be filed within four years. The four bad actors worked in General RV’s Draper, Utah, dealership from 2014 to 2017. None of the crooked paperwork falls within the four-year statute of limitations, and prosecutors simply can’t pursue the mechanics of this shyster-swindle. No charges can be filed.

What help for victims?

Where does this leave the victims of this sleazy scam? Stepping up to the plate, credit unions across the Beehive State, when they heard of the matter, started an audit of all loans connected to General RV. They found dozens of cases of “discrepancies” and reported them to the DMV. Then, to their credit, they worked with members who got stuck with unexpected balloon payments to work out suitable refinancing.

For Lisa Pueblo, the refinancing efforts may have been a relief. But for the General RV employees who created the mess in the first place to have no charges filed against them? “They should go to prison,” she told the local FOX affiliate that first broke the story. “I mean everything about it was wrong! … I just think it’s so deceitful for these salesman to do this. It would be amazing if their names came out, and buyer beware!”

Utah DMV’s Shinney says that the one who he thinks “masterminded” the crooked affair is now completely out of Utah. As we said, none of the four work for General RV anymore. But interestingly enough, some of the scammers work in – guess what? – the finance industry. Buyer beware, indeed!

Protect yourself

So how can you protect yourself against a scam like this one? Before you sign on the dotted line on a loan contract – or any other legal paperwork – make yourself unbearable to the finance manager. Take the time to scrutinize ANY and ALL paperwork you’re asked to sign. Don’t accept the standard malarkey of, “This is just customary paperwork, sign here.”

Does the paperwork have “carbon copies”? Be sure to examine the data entered on each copy to make sure it all matches up. If something doesn’t “feel right,” then STOP, take copies of the paperwork with you, and get someone (potentially an attorney) to help you go over them, before you return to sign them. If the dealer won’t let you take the papers away, don’t walk away – RUN away.

Check any current loan papers – just in case

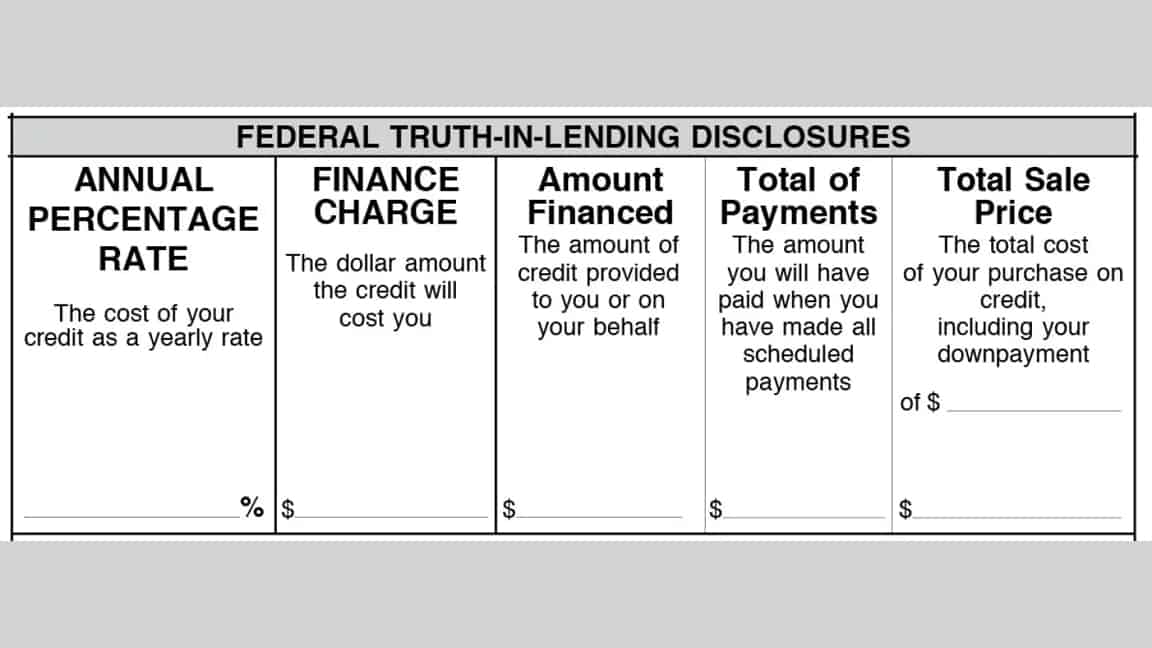

While this scam appears to be limited to General RV, it may not be a bad idea to take out any active loan papers you have and give them a good look-see. Federal law requires that any loan contracts have a clear, fact-containing box up at the top. The numbers in the boxes disclose the number of payments, the amount of each payment, and the finance charges. Then the last one, the total of all payments. Take out your calculator and do the math. The numbers should all add up.

Utah’s DMV says that General RV cooperated with their investigation. That may well be, but it could take a while for the company to re-earn the trust of the buying public, while four of their former employees walked away from crooked dealing, all with no charges.

Ever felt like you’ve been victimized by an RV dealer? We’d like to hear about it. Please fill out the form below and enter “Potential Fraud” in the subject line.

Related

Utah RV dealership customers say they’ve been cheated

##RVT1026b

Those crooks should still be prosecuted to the fullest. I bet they are still working in the RV business somewhere. Thank you to the credit union that stepped up.

I agree but due to statue of limitations, they can’t. Laws are legal but not always practicle.

When we decided to buy a C class we stopped at Freedom RV in Marana, Arizona. When we were handed off to the “Deal Guy,” one of the first things he said was “Give me your credit card.” We couldn’t get out of there fast enough!

I’m glad other lenders have stepped up to help out these victims. But honestly, Chuck has preached for years to beware of these 20 year loans and steer clear. His reasoning of course was that the buyer would be underwater almost immediately. Reading Chuck’s warning, I realized I had a 20 and seeing how ridiculous it was I have paid extra each month and will pay it off early next year 15 years ahead of time.

I would hope authorities would follow up on those crooks and look at what they are doing now. Likely they could find more fraud within the 4 year limitation and charge them.

I don’t understand how the employees benefitted in any way. The bank held the loan. They got the early payment. What’s in it for the “crooks”. And 119 payments is pretty clear to me

Thanks DougV. I was going to bring this up. Nowhere does it say these charlatans got any money off this scam.

Presumably they got a kick back from the bank.

I presume it helped them sell the RV, resulting in earning a commission that would have been more difficult to earn without false favorable financing terms.

Marianne Edwards, you are 100% right!☮️✌🏻

Most of the loans were financed through credit unions. Generally, dealers steer financing for their sales to whichever financial institution is easiest to work with and which pays the most in “rebates.” As they say, “follow the money.” My guess is they changed the paperwork to obtain the largest “rebate” from the financial institution. The financial institutions involved all readily “resolved” the issues with the consumers involved. Here in Utah, it’s very business friendly — which is why (I’m guessing) the local financial institutions involved were not investigated nor held responsible – certainly not by the local Fox TV channel that broke the story. General RV, of course, is not headquartered in Utah.

If nothing else, commissions they might not have gotten without fancy shuffling.

It’s unfortunate that they don’t teach about finances in school. For several years my father taught a night school course on finances because he was tired of seeing people get ripped off. He was the general manager of a large credit union and did it unpaid as a community service.

Your father was a good man Colin!!!☮️✌🏻

I know a young couple that bought a house with the same type type of contract. A 20 year mortgage that did really clearly explained how the balloon loan worked and that the interest was not being charged for the first 10 years. That interest was tacked on for the final 10 years almost doubling the payments.

It was their fault for not researching the type of loan they took out. And of course the finance company did not explain it. They lost the house.

A decent bank would have sent the papers back to the dealer and told them to do it again without smudged numbers, unless someone at the bank was working with the people at the dealership. Years ago we were getting a mortgage with a discrepancy about escrow and we made the loan officer show us her paperwork. It had a glob of white out on a photocopy. She of course denied that she had anything to do with that, but she did get the paperwork replaced. In retrospect, I wish I would have raised more hell about it.

I would never buy anything from General R.V. or Camping World, not even a light bulb. Just slippery crooks wearing nice clothing kindly stealing everyday people’s hard earned money. There are plenty of honest, family owned R.V. dealerships out there that deserve your business. Read the reviews, and leave good, honest reviews as well! Need a repair? Try a mobile R.V. repair service as well. Once again, read the reviews on Google or their website. And leave a accurate honest review, good or bad!

There’s definitely an advantage to paying cash.

How did they profit by doing this?

They distributed it among themselves and the f&i manager had to be aware.

What was the motivation for them to do this? I wonder, since we don’t know their identities, if they are currently working for other RV dealerships in Utah?

The motivation was likely getting the monthly payments to reflect what the customer wanted to pay. The full term loan probably had a higher interest rate and higher payments. Do a shorter loan and the bank will likely give you lower interest but larger payments. Thus, having one huge payment in what would be the discussed loan time means you’re technically taking out less “money” for the vehicle and will pay the remainder at the end of the agreed timeframe.

I personally (intentionally) purchased a car this way. 2yr 6mo instead of 5 year loan. I made larger monthly payments so when the 2 1/2 years was up I had a single large payment to make but still less than what was in my loan documents.

Other than the impossible to pay ballon payment, how was anyone hurt? The buyer saw affordable monthly payments and snapped it up. The buyer didnt look at the whole contract. I bought my first house that wY. Five years in , one BIG payment, which by that time I had equity in the house and was able to get a conventional home loan. If anything, they helped me.

Someone didnt do due diligence. Now blame someone else.

I don’t think most people would ever think to look at every copy underneath the original- that’s a slimy trick.

This was popular in the ’70s. People were hoping houses went up in value to cover their butts. Something went wrong and they went out of style. Banks and people lost a lot of money. Then came the adjustable interest rates which again caused people and banks to have problems. The finance world is always coming up with ideas that can cause problems later.

Certainly not to condone this practice – however, did anyone read the contract and purchase agreement? BEFORE signing it! This used to be way to buy a car years ago. “I can afford the monthly payments and in 1 or 2 years, I can refinance it!” Pretty dumb – but it is about the “monthly payment” – not the total price in the end! Thus comes a new “Truth in Lending” law – but you still have to READ the contract before signing……

15 years ago, I was In-Contract to buy a house. Took the time to read the entire document. Found a line in where my real estate agent would get extra % monies, over the standard percentage. Went and asked the question, if I understood this correctly.

You can not imagine the uproar my question caused. The main agent came out of his office, and began making phone calls to my agent, and demanded to know why this was in the contract.

This knowledge comes from being in the real estate appraisal business and taking and understanding finance courses.

the people who write the loans (sales people or the “F & I” manager at the sales office, make money on the finances amount from rhe banks or paper holders. The sales person will make a percentage of the loan amount when the loan document is “sold” to the finance company after the loan is seasoned. That means after you sign the loan documents, the F & I person markets the document to the company that will pay the largest bonus or commission, and then the loan is in existence for more than a pre-determined time period. It happens all over, loan companies, car finance companies and almost any other company or broker that sells the loan. If you want to fme nance a purchase, go to your bank, a mortgage BANKER, not broker or your credit union. Most of these are honest and by law will provide the “truth in lending” statement. If not, run away!

While I agree that the sales people acted unscrupulously, I have just one question for the “victim.” Can the buyers not do simple addition and multiplication math??? People taken advantage of in these situations get taken because they did not exercise the personal responsibility to do the math and make sure the finance people could document in writing that is then part of the contract EXACTLY what is owed and when. These victims accepted and signed off on flawed paperwork so, in effect, they were complicit in getting the shaft!

PBB

That’s just it. The math of their payments to the number of payments likely added up.

What it came down to was likely that they couldn’t get the loan approved for price, and number of payments to equal how much the customer was willing to spend. So they doctored the loan to make them pay the last half all at once. But the bank was likely wanting larger payments or shorter loans. So they buried the details in paperwork that most people fill out maybe once every 5 years.

I too wondered how the “crooks” could have benefited from that change in the transaction. Probably some financial aspect I don’t know about, but I’m sure that, somehow, they did. It’s pretty obvious from the photo provided that the number of payments was altered. Unfortunate that the statute of limitations prevents any further action.

We bought our first-ever motor home in 2015, but thanks to valuable advice from sites such as this, I was very aware of how quickly buyers could become “upside down” in their loan. As a result, we worked very hard to pay off ours early (done through a home-equity line of credit).

Yes, we had to scrimp & save, but now we are the sole owners of a 2015 Roadtrek SS Agile after 5-1/2 years. Glad we were prepared. Keep giving good consumer advice!

I’m guessing they couldn’t get the loan approval for the RV at the price the customer would accept so they doctored the payments to make it all look good to the customer. They benefited by getting sales “completed” for their commission checks most likely.

Like a home mortgage with a balloon payment, the buyer got a lower payment, so the seller was able to entice them with a lower payment, but didn’t tell them about the balloon payment.

I don’t understand someone who purchases a RV and has to make years of payments on a unit that will lose its value. Either save up and buy one or get something used that you can afford. That’s what we did.

That’s what you came away with from this article?

So you saved up to buy something that would lose value? That doesn’t make any sense either. Any way you do it, the asset is going to lose value.

Buy an RV burial plot at the same time you sign the papers that way you will have a place to stick the RV at the end of the twenty years. It will be junk in 20.

The victims may have some recourse under federal law. Violations of the truth in lending act are investigated by the FTC and Office of the Comptroller of the Currency (OCC). The State of Utah’s statute of limitations may have expired but then a complaint with the FTC and OCC should be initiated.

I worked at a used car dealership for 4 years. I delivered cars out of town quite often.

I always offered and most of the time encouraged customers to look over the paperwork before signing. Some of them would look at me funny but I would explain that after a decade in the military I am an avid proponent of being sure of what you sign. I told them I would answer any questions I could or I would get the finance person or boss on the phone for any questions I couldn’t answer. I delivered well over 200 vehicles in those 4 years. Only 5 or 6 times did the paperwork not match what was agreed upon. Only 1 of those times did the customer not complete the paperwork (after being corrected) and we didn’t get the sale. My key thing to have them look over was the interest rate, number of payments, and amount of payments.

If I remember correctly I thought the contract was changed after the couple signed all the paperwork and left with there new RV

I would be interested in knowing if the buyers’ copy of the sale paperwork was the same as the store copy…..did the amendment to the # of payments happen after they signed or before? If before, and the buyer didn’t comment or notice the smudged number of payments, then they do bear some responsibility for their error. But if their copy shows 240 and not the smudged number, then it floors me to even consider that the dealership could get away without being charged or punished somehow.

What does General RV have to say for themselves?

I have purchased a lot of new vehicles in my lifetime. Many years ago i agreed to a 36 month term on a contract and it wasn’t until 2 years later I realized the Dealer changed the term to 42 months. Cost me an extra 6 months and $1800 in payments. When I reviewed the paperwork I just looked at the payment amount. Totally my fault for being excited to sign and drive away in my new car. Since then I carefully scrutinize the payment, term, and total to make sure they add up. Two times since I first got scammed I found the number of months were changed on the contract from what we agreed on, once from 48 to 52 months, and once from 72 to 75 months. Both times the dealership exclaimed, “oh thats a typo” and changed it. So it’s happened to me 3 times in 30 or so purchases. I can only imagine how many times this happens in this country.

I have long believed that a sales contract for an Auto, RV, or home should have copies of the salespersons drivers license, just in case something goes wrong.

The ultimate protection is don’t finance depreciating assets. I haven’t had a car payment since 2008, I had bought my first 06 300 in 07, loved the car but got tired of the $425/month payment plus full coverage. Sold that and bought an 00 Cadillac SLS for $2800 (middle of winter, no climate control fan or it would have been $3500) Checked the Cadillac dealer, $700 to replace, had a Seattle auto wrecker drop ship me a fan for $50. Found a one owner, almost exact clone of my 06 300 in January 2016, dealer was asking $6995, I paid $4412 including tax and license, being January, after Xmas, before tax money and I had cash. Bought the wife’s 07 W.P. Chrysler Signature Edition AWD as an Xmas present, they were asking $4K, they let me take it and do a full diagnostic, I came back with everything big and small, didn’t embellish and the costs to sort everything out. Anyone purchasing that car would not have been able to afford to fix it. I offered $2500 figured they would call in a month

Instead they said bring cash, they even included tax and license in that. Car is completely sorted mechanically and well on its way appearance wise 👌. Only credit I use is my mortgage 2900 sq ft 4 bed 2 bath, $497/month including taxes and 1 credit card for my car stuff

Good article. But I had to smile seeing a GMC on the card.

The customers should be able to go after the individuals that perpetrated the scam individually and make them financially responsible for this fiasco, put a stop to their criminal enterprise, permanently, when their homes are foreclosed upon for having to pay these people back!😤🤬🧟♂️🤦🏽♂️🤯🦃

But what is the actual malfeasance? Are they getting a larger kickback, allowing people to qualify who otherwise wouldn’t, fudge the numbers so the payments appear affordable?

I wouldn’t buy a RV or anything from that company no matter what. What a shame that they couldn’t do the right thing. General RV should be better.

RV dealers and builders are not to be trusted. They can spot a sucker a mile away. If there lips are moving”””””””

Ok but what is the scam? Is it a larger kickback from the financing company? Does it make it possible for some people to qualify who otherwise would not. Personally I am all about cheap and cheerful. When my kids were young (2002] we bought a 24′ trailer made in 1977. We live in the desert so no water damage, just faded paint. When you opened the door it was like going back in time with wood paneling, orange and brown curtains and upholstery, yellow vinyl flooring, brown appliances. Thing was immaculate inside, I replaced the gaskets in the water system, hooked back up the water heater and hot showers. there was a full size bed above the mom and dad bed, also full and the table and benches make a twin, slept 5 easily. Even the roof AC worked. Bought it for $1350, after using it for 3 summers of cheap and amazing vacations I sold it to a guy as his hunting rig for $1800. Why anyone would finance anything like that is beyond me, I haven’t had a car payment since 2008.

Ran out of room, my only loan is the mortgage on my 2900 sq ft 4 bed 2 bath, full finished basement, large front and back yards (10K sq ft lot) and a big garage for my projects. I pay $497/month including taxes.

There’s an ancient Chinese saying for things like this: “Caveat emptor”… 😉 I think folks have gotten too used to just hurrying past the disclosure verbiage of online service agreements and clicking their mouse. They gotta slow down and go back to “reading the fine print”…and asking clarifying questions!

Well, heck, Carson. And here I always thought that was a Latin saying. Does that mean carpe diem is also Chinese? 😆 Have a wonderful Thanksgiving, and don’t forget to carpe the turkey. 🙂 –Diane