By Chuck Woodbury

Every week, it seems, more national parks only accept payments by credit or debit cards. Have you ever considered what a bonanza this is for Visa, Mastercard and the countless thousands of banks around the country that issue and profit from those cards?

If you were a banker or credit card executive, wouldn’t you be thanking your lucky stars for this cash cow that just keeps on giving?

Business intelligence company Nilson reports that the largest portion of fees that you and I and others pay at national parks from credit card usage goes to card-issuing banks, card networks like Visa or Mastercard, and “acquirer” banks or a third-party processors.

The Merchants Payments Coalition (MPC) cited findings from payment consultants CMSPI that showed in 2023 that the swipe fee rate for Visa and Mastercard credit cards averaged 2.91% of the transaction amount (we at RVtravel.com pay a little more than that).

Some of national park entrance fees go to credit card companies and banks

And so when you use a credit card to enter Yellowstone or Yosemite ($35 admission in both cases) or many other national parks, some of your money goes to credit card companies and banks. What a sweet a deal for them! But what a crummy deal for park visitors whose dollars are diverted to corporations that have no direct involvement in operating, maintaining or improving the parks.

Yellowstone and Yosemite, alone, draw about 9 million visits a year. So when you use a credit or debit card to enter or camp at these two national parks or 50 or so others, the bankers dig their claws into the till and grab some of the booty for themselves.

The national parks have accepted and even relied on card payments for a long time, so you and I have been paying these outsiders all along. But paying with cash was still an option, so the banks didn’t profit from every single visitor. The parks say it’s more efficient for them to process “plastic” than cash, and that they save money in the long run. That may be, although tough luck for people without a credit or debit card.

There has to be a better way.

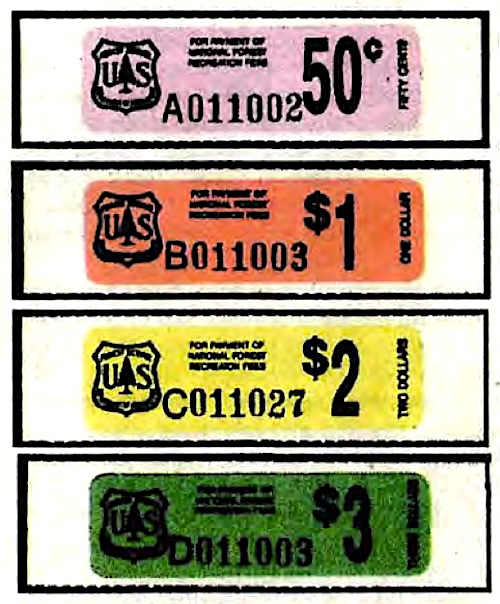

Camping stamps were a great idea

Here’s an example of how we Americans were once more creative, even federal bureaucrats. In 1985, the U.S. Forest Service began selling camp “stamps.” A prospective camper would purchase them in advance from Forest Service offices. They could purchase, for example, $100 of prepaid camping credits for $85, a 15% savings.

At the campground, instead of dropping cash in a small envelope (which was subject to theft), campers used their prepaid stamps, which fit into wallets and purses. I used these for several years. They were very handy and saved me considerable money over time. I liked that a sticky fingered seasonal employee could no longer pocket a fee envelope with my money.

Senior citizens, who already could camp for half price with federal discount passes, would save even more with the additional 15% stamp discount. Some critics thought that was too generous.

How the program evolved

The primary benefit to the Forest Service from the stamp program was the significant savings in administrative and accounting costs since dealing with cash and checks was no longer necessary. Before the stamps came along, on Monday mornings, fee envelopes with cash and checks would be delivered to ranger stations. After a busy weekend there might be a huge pile: each one had to be opened, processed, counted, recorded, and deposited at a local bank. In ranger districts with moderate to heavy recreation workloads, the envelopes were collected several times a week.

It was quickly determined that using “Camp Stamps” significantly reduced the workload of collecting fees; the time and effort saved easily made up for the loss of the 15 percent discount. An additional, unintended benefit was discovered by one Forest Service region. It determined that 18 to 20 percent of the stamps sold were never redeemed, which translated into extra revenue for the government. In 1987, the stamps accounted for 11.3 percent of total user fees. The ultimate goal of the program was to reach at least 50 percent.

The program did not last

Alas, the program did not last. Concessionaires did not like the program because they earned less, and many Forest Service bureaucrats couldn’t get excited about it. Others were too busy to spend the time necessary to learn the new program and its financial procedures. Others simply did not like change. I remember at the time being sad the program was ending.

And yet the goals of the Cash Stamps program were almost exactly what the National Park Service is trying to accomplish today, except nobody back in the Camp Stamp days was cutting banks in on the action. And so I ask, isn’t there a better way, today, to collect fees from national park visitors without handing over millions of dollars each year to bankers?

There’s a way, I know it. But how? Any ideas?

RELATED

- Top 5 national parks stay mostly open; details sketchy

- What RVers need to know about national parks and possible shutdown

- How a government shutdown could affect your RV trip to national parks

- Visitors may not see the strain, but national parks are operating with thinner teams

- National parks face devastating cuts, with majority in jeopardy

- Interior Secretary orders national parks to stay open amid staffing cuts

- National park visitors face reduced access and services across the country

RVT1229

Maybe require a donation from the banking company? They are always making donations to get tax write offs anyway. At least this would help the parks.

I think that the banks, through their lobby, have already made a donation, in the form of campaign contributions, to the people who are instituting these policies.

Well they said fogitaboutit ain’t no happening ever

Not only are we paying banks interest, but when we use some restaurants or merchants they tack on a additional 3% to our bill. Many poor people can’t get credit cards. Our government agencies tell them to get Visa or Mastercard gift cards which cost the purchaser $7. or more. Wonder how gift cards for restaurants and merchants work. Financial institutions also have to pay the credit card companies a fee for the right to issue credit cards. Senator John Fetterman is supposed to do a bill to force those who accept credit cards to accept cash for under I think the amount was $500. I like to pay cash, so I hope it goes thru. I’ve been at function that would only accept cash for food or a bottle

Consider that the banks have to pay their employees and rent. Also, all those perks like cash back and miles, etc. We pay for other conveniences every day, like maybe a little extra for a pull-thru site. What is so bad about paying for this convenience?

Kelly, With your “Pull Thru” example, the camper makes the choice to pay the extra fee for the convenience of a Pull Thru. Otherwise, they can save a few dollars and learn to “Back In”.

The issue that the author is making allows for no choice on the part of the park visitor, other than “Go or Don’t Go”, because that park will ONLY accept plastic (with the attached fee).

When I buy something at a convenience store, and they tack a 3% fee for using my credit or debit card, I still have the “cash or charge” choice, because they will still accept my cash. NPS will not. That’s the issue.

I don’t mind (occasionally) paying a little extra for a pull through site, but the point is I get to choose. Pay a little extra, or back in. The author’s point is that the NPS gives the visitor no choice, other than “Go, or Don’t Go”. The park will not accept their cash.

With a pre-paid card exclusive to the U.S. Government (and in-park concessions) for recreation. For those who wish to, they could even buy and fill the card with a credit/debit card.

But you’re still losing the 3 percent for using that card because you’re paying for the use of the card reader technology. And the government is not going to give anything for free.

This ship has sailed. I believe that this is about the “Credit Card Lobby” getting their rewards for heavily contributing to the election campaigns of either side. Remember back when they convinced Senator Biden to sponsor, and subsequently pass a bill that disallowed credit card debt from bankruptcy discharge? He didn’t do that out of a moral duty. I think this is along those same lines.

Also, the Government has been creeping to a cashless society for some time (digital currency). These federal agencies are simply following that agenda.

So, as an example, say your $100 purchase of the camp stamp costs $85. So the FS gets $85 to run the campground That’s 15% less AND what if the person paid for the camp stamp with a credit card?. That same $100 paid with a credit card will cost the FS 2-4% or $2 to $4. That means $96 to $98 are available to the FS to run the campground. The larger the entity the better the rates are that can be negotiated with the CC companies. I’m not a big fan of CC fees. I had to pay them when I ran a business, but it WAS/IS the cost of doing business. And in this case, it appears to be a less cost of doing business.

“the bankers dig their claws into the till and grab some of the booty for themselves”. C’mon Chuck, do you really think that’s a reasonable and measured observation? Credit card use is ubiquitous in our society for real sound reasons. They allow convenience and ease of payment, and there is a cost for that. There’s also risk involved and also a cost for that as well. If this is your thesis on National Parks, why not go all in and criticize cc use for everything?

“If this is your thesis on National Parks, why not go all in and criticize cc use for everything?”

Because the vast majority of vendors give the consumer a choice of “cash or credit”. Chuck’s point is that the Gov’t is giving the visitor no choice. Well may the choice to either stay home, or use the cc.

But the CC companies/banks didn’t mandate their card use, so why make it sound like the “greedy banks” are almost stealing?

I agree with Larry. The statement and it’s intended purpose, was out of line.

I am not a proponent of the NPS refusing cash. Our own gov’t shouldn’t have a policy of refusing its own currency. But I don’t blame bankers for a policy the NPS involked.

Found this on the web: The National Park Service (NPS) is going cashless to improve efficiency, enhance security, and maximize funds for visitor services. This shift reduces the time and cost of managing cash, minimizes the risk of theft, improves transaction speed, and creates greater accountability for fee collection. Visitors can pay in advance on Recreation.gov or use electronic payments like credit and debit cards at park entrances, with alternative options available for those who cannot pay electronically.

As a retired CPA, I agree with the points made in this post. The credit card fees are a much cheaper process to use than trying to manage actual cash, which takes a lot of time and effort behind the scenes.

That and a lot of people can’t make change anymore.

Actually, more and more Federal campsites are requiring you to use Recreation.gov, a PRIVATE COMPANY, to make reservations and even pay for first come sites. Funny, people are complaining about the NPS having to pay 3% to a credit card company yet are completely silent about the camper having to pay this PRIVATE COMPANY a service fee each time you make a reservation. And now you HAVE to pay this service fee just for camping at a campsite.

Agree. Managing a separate website for reservations would also be costly. Not sure what the cost/benefit analysis of that one is. All I know is that in general, public or private, those reservation fees can be a big % adder to a single night stay!

Yup. We like to move around, especially when we are “exploring.” It’s terrible having to pay that “processing” fee every time we move. Maybe REC.gov should charge a percentage of the total cost rather than a flat fee.

So, you want to hear a good one? We made a reservation at a National Forest campground that had to be made through Recreation.gov. They charged us $9. A month later, we got an email from them stating the FS was going to remove a culvert and build a bridge on the road to the campsite. The road would be closed.

I called the local FS office and found out I could still get there but had to drive about 60 miles more, 20 mile of which was on a gravel one-lane forest service road that would also be being used by a bunch of logging truck. They were being re-routed on that road due to the road being closed. So, using Recreation.gov, we cancelled our reservation. Recreation.gov charged us $1

Charged us $18, $9 to make it and $9 to cancel it.

😵💫🤯

What about the $8.00 reservation fee? I do not like this extra cost, rather negates my senior disabled discount.

One of the problems with cash is it could be counterfeit, or checks may not have enough in their bank account. With credit cards, the bank is checked during the transaction to determine whether the account is satisfied during the processing and would reject a card with insufficient funds. I also would be told the credit card was stolen and told to hold the card.

When I had a business, I posted “Credit Cards” have an additional bank service charge. My employees would not take a discount if the payee used a credit card!

As a camp host in remote dispersed National Forest campgrounds, we can only accept cash or checks. (This is because there’s no electricity, internet or cell service to run a system, and if there was a system, it would be vandalized or damaged by weather.) I can testify that processing paper envelopes and their cash or check contents takes a lot of time and expense. Labor hours for unwinding visitors’ wet crumpled bills, checks written out wrong or damaged by rain and not accepted by the bank, fuel to deposit funds in a faraway town, etc. are all expenses. Credit card processing fees seem reasonable in comparison.

Get a National Parks senior pass and never pay entry fees again.

You still have to pay for camping.

Chuck, you crack me up.

Unlike “the good old days” when we forced every location to employ an NPS employee to drive to the bank to deposit Traveler’s Checks, Camp Stamp proceeds, cash and hot checks, e-transactions are far more cost efficient.

Yeah, the bank scrapes some income to cover the costs of the software and their servers plus costs coupled with dispute resolution, identity theft and charge offs but is 2%-3% truly unreasonable?

I think paying Booz Allen Hamilton an $8.00 service fee to be on the other end of the transaction is where the real crime is. 3% of a $40.00 camping fee is $1.20. I’ll let you do the math on how many percent $8.00 is….LOL

Because dealing with stacks of cash and buckets of change costs nothing so there’s no expense to pass on… oh, wait…

And no, we weren’t “more creative” in 1985. Then, like now, we did what was the most convenient. In 1985 credit cards still required an imprinter and paper receipts. Today, they’re completely self serve.

Do you have any idea how naive your complaints sound. Yes, financial.institutions make money of every credit card transaction and have for years. It costs money to provide you the cashless convenience. Those networks and systems don’t build and maintain themselves. Yes they make a profit but they are a business.

Although I’m no fan of paying banks more, you talk as though there are no costs associated with taking cash. For example, those armored trucks and armed guys that take it away aren’t free either. Also there is plenty of overhead to deal with the stamp paradigm as well.

Chuck, I agree, CC fees drive me nuts. Having read thru all of the comments I thot about the vending business I once ran. I had a safe on each route truck, a large one in the office for a days worth of coins, a coin counter with half time person to run it, dollar change machine’s to maintain, and Brinks fees to transport to the bank that then charged to handle all the coins. Today when you put a dollar bill into a vending machine, the computer back in the office knows it right away and it is posted to the books for that individual machine. All above has been eliminated plus no more machine break-ins and repair costs. Maybe card fees and computers do save money? A changing world for me too.

This is why you buy your pass online. Then you’re only paying the card fee one time instead of at every park station you visit. I think it’s ludicrous that the banks want you to have the convenience of using a card instead of carrying cash, but then turn around and make you pay for that convenience with a 3 percent fee even on debit cards.

Yes it is. If you don’t like it, move on and quit bitchin

It’s bad enough you have to pay fees to get into national parks already funded by our tax dollars then use only cards to pay them. The big money lobby seems to be running this country & getting rich off us all.

They’re called “Interchange Fees” and they are typically 2.5% to 4% depending on…. factors.

The question we all should be asking is, “Why is it that Interchange Fees in Europe are capped at a hard 0.3% for credit, and 0.2% for debit card transactions?”

Could it be the bank lobby has our Congress by the short’n’curlies?

FYI: I’m a former bank employee; I know lots of ways the deck is stacked against the little guy.

But they do have a direct involvement in operating the parks. Collecting payment is an operation of the park and Visa is part of that operation. Are you going to go after Microsoft for profiting off Windows that is in the Rangers computer. You want to talk about a real killer – let’s discuss IBMs service fee for use of their decades old Maximo software used to manage and track inventory and maintenance work. Hundreds of millions per year the NPS pays just to access a website that they have to host and maintain.

First world problems.

Better question is it “right” for merchants to pass on the credit card fees to consumers? It’s a cost of running your business so include it in the price or do they want to make themselves just look good. “It’s not our fault they charge for borrowing money”

I have the Senior Lifetime Pass. My wife and I get entrance using this. We are full timers so it has paid for itself easily.